One person in four becomes incapacitated for workDisability insurance

Imagine that suddenly you have to get by on just one third of your current income.

Consumer advocates warn that next to personal liability insurance, disability insurance is the most important form of insurance.

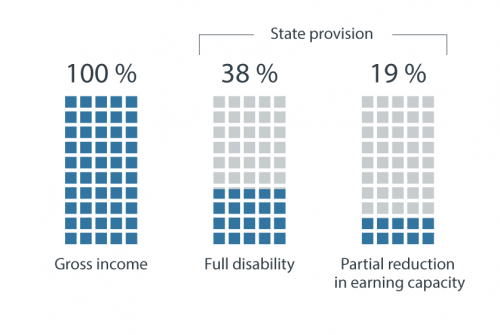

Loss of the ability to work is a risk that threatens financial existence. No longer being able to work often means material hardship. In this serious situation, the state does not provide much help: Starting from year of birth 1961, the statutory pension insurance scheme only pays a mini pension in the event of total disability.

Disability can affect anyone

Every year, approximately 180,000 people are forced to leave their professional life for a longer period of time, or leave it completely because they become ill. Statistically, every fourth employee is affected by this fate. Often, everyday illnesses are the trigger factors.

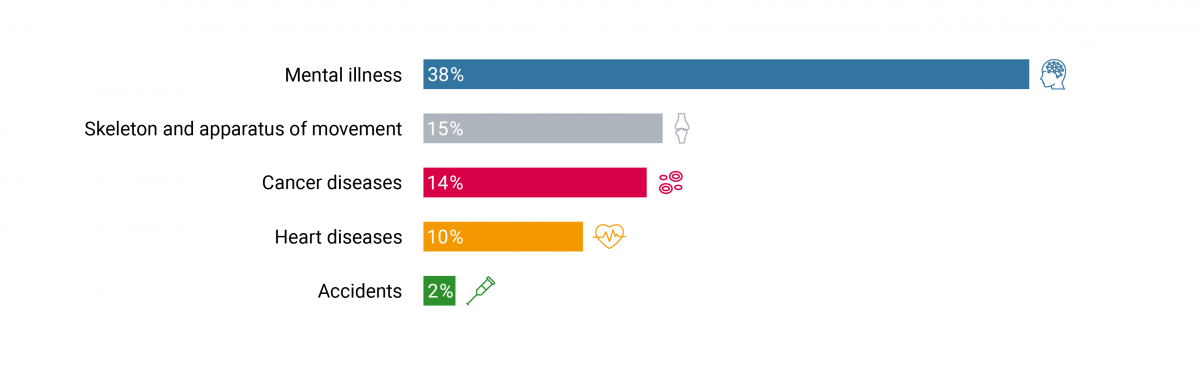

The most common causes: Psychological factors, back, cancer

Anyone who think they are not affected is wrong: Every job is risky, even an office job. For many employees severe chronic back pain develops as a result of the sedentary activity. Others suffer from stress-related psychological and nervous problems. Accidents are the cause of occupational disability for only one in ten people whose lives are thus impacted. In most cases, premature termination of employment causes fa-reaching everyday problems.